The Indian Economy

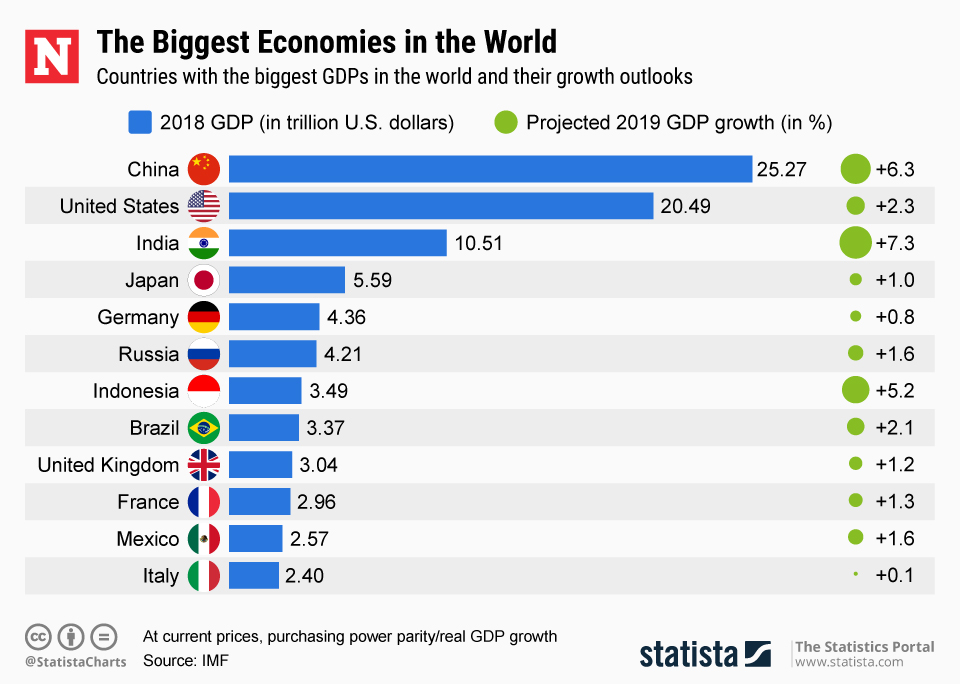

India has the third largest economy in purchasing power parity terms valued at USD 10.2 trillion. With over 500 million work pool, India has the second largest labour force with the second largest female technological workforce. According to Angus Maddison’s study on world economy, in the last 2,000 years, India was the largest economy for 1,500 years and then the second largest till 1800 till the British set up the Raj. When India gained independence, its share of the world economy was 3.8%.

Expanded economic presence in Russia’s Far East

India is planning to bolster its econmic prescence in Russia’s Far East. During the 2019 visit of Indian Prime Minister Narendra Modi, India annoucned a USD 1 billion loan to aid the region’s development. This development gels well with Russian plans as well.

Continue readingMultipronged foray to meet 2030 sustainability goals

India is collaborating with many countries to generate 450 gigawatts(GW) of renewable energy by 2030.

Continue reading

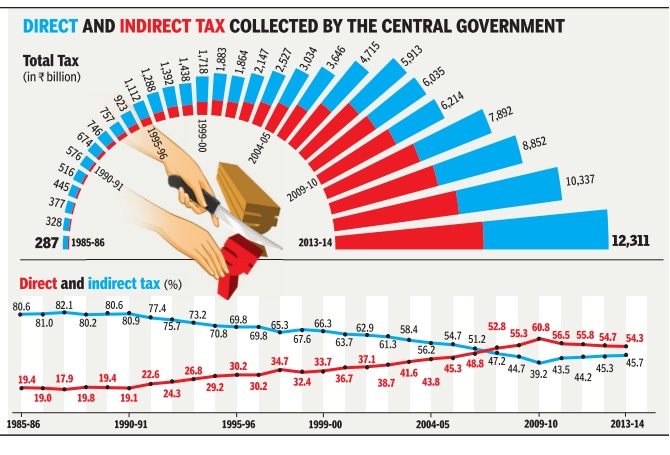

India has the third largest economy in purchasing power parity (PPP) terms valued at USD 10.2 trillion (USD 3.05 trillion in nominal terms and ranked sixth by this measure). About 60% of the economy is due to private consumption and rest from government spending. India is the ninth-largest importer and twelfth largest exporter. With over 500 million work pool, India has the second largest labour force with the second largest female technological workforce. The country also has an almost equivalent informal economy that operates under the radar of measuring mechanisms but direct tax rates have been growing while all citizens pay indirect taxes through Goods and Services Tax (GST).

With over 500 million work pool, India has the second largest labour force with the second largest female technological workforce. About 34% of the population is under age 14 and 60% is between 15 and 64 and 4.6% is over 65. More significantly, about 41% of its population is under 18 years and about 48% under 21; meaning a significant portion of its population is ready to enter the job market. About 45% of males and 44% females are married. The percentage of divorce or separation in India is very low-- .3% for males and .2% for females. An International Labour Organisation report, something to be taken with a pinch of salt, estimated that India’s informal labour was at 81% of the total pool. According to government statistics, only 12.5 million people are employed by large industries and 120 million are employed by micro, small, and medium enterprises (MSME).

For millennia, India was the largest economy in the world at one time owning more than 50% of world’s assets. According to Angus Maddison’s study on world economy, in the last 2,000 years, India was the largest economy for 1,500 years and then the second largest till 1800 till the British set up the Raj. Between 1700 and 1900, Maddison found that India's share of global industrial output also declined from 25% in 1750 down to 2% in 1900 and its share of world economy 24.4% to 4.2%. Thereafter, the British systematically dismantled Indian industries so they can export the raw materials to Britain and buy back finished goods from it. When India gained independence, its share of the world economy was 3.8%.

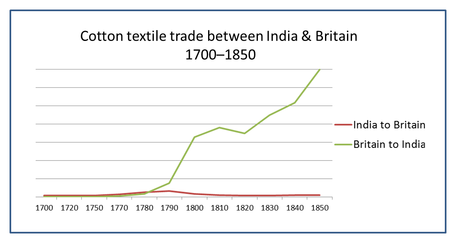

When the British defeated the Marathas (who had earlier defeated the Mughals), India was the largest cotton and textile producing nation in the world in addition to silk, rice, and other much-in-demand products. In order to destroy the textile industry in India, the East India Company (EIC) cut off the thumbs of all weavers so the cotton had to be shipped to Britain, made into cloth, and exported back to India. At that time, real wages in India were more than that in Britain and had to work fewer hours. Further, there were no import duties into India virtually giving British companies a monopoly in India. So, in many ways, the EIC must have felt it better to destroy the industry here to sell British finished goods to the market. Additionally, the British also destroyed handicrafts, metal works, agriculture, and other industries.

After the British Raj was set up in 1858, things worsened. A flat 10% of the total national income was automatically transferred to Britain. With declining industrialisation, Britain made India a net importer of British manufactured goods and exporter of tea, coffee, oil seeds, foodstuffs and other industrial raw materials which were considered essential for running British industries in England. European officials and non-officials repatriated their profits immediately to Europe so there was no capital reinvestment in India. European companies also repatriated profits and interests on loans depleting available capital even more.

Realising the quality of labour now relegated to abject poverty that the population was unused to, the British also exported labour to major parts of the world as indebted labourers—Fiji, West Indies, Africa, etc. Paid but essentially treated like slave labour, this workforce produced more raw materials needed by the growing British economy. The taxes collected from India and its colonies funded all British wars, Indian soldiers gave their blood for their colonial masters. Worse, it instilled a sense of uselessness through its schools magnifying any defects in society and attributing them to the native religion and glorifying small achievements of the Empire.

They spread canards about the caste system when in fact, the so-called lower-castes were well off compared to their European peers. For example, out of 62,048 landlords in Thanjavur, only 17,149 were Brāhmaṇās and 1,457 were Muslims. The rest were the so-called oppressed classes. In many ways, it took Indians almost 70 years to sort of break out the colonial slave mentality.

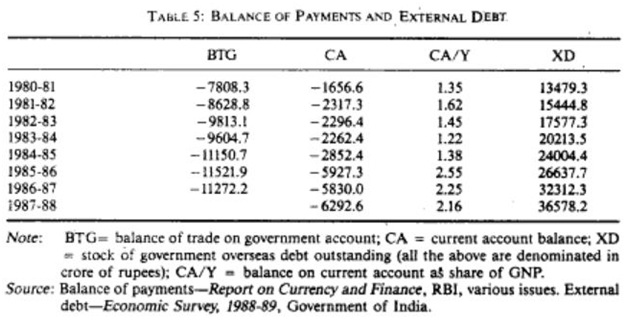

After independence, the country under Jawaharlal Nehru was keen to bring a socialist form of economy where centralisation and big government was the emphasis. This Soviet and Nordic-inspired model resulted in suppressing industrialisation and competition. The License Raj promoted protectionism and corruption and continued till early 1990s when the country faced a balance of payment crisis forcing it to eschew decades of regressive policies and open up the economy to private players and foreign investment. From 1947-1991, the Net National Product (NNP) hovered between USD 500-1,400. After liberalisation, the NNP has grown 328% to over USD 6,000. The Indira Gandhi era was modelled predominantly on the Soviet model. The Rajiv Gandhi years were mostly responsible for the balance of payments crisis early 1990s because of excessive borrowing. The Indian National Congress also withdrew support to several governments that followed and hence threw the country into a decade of minority governments without any power to make structural changes to pump up the economy.

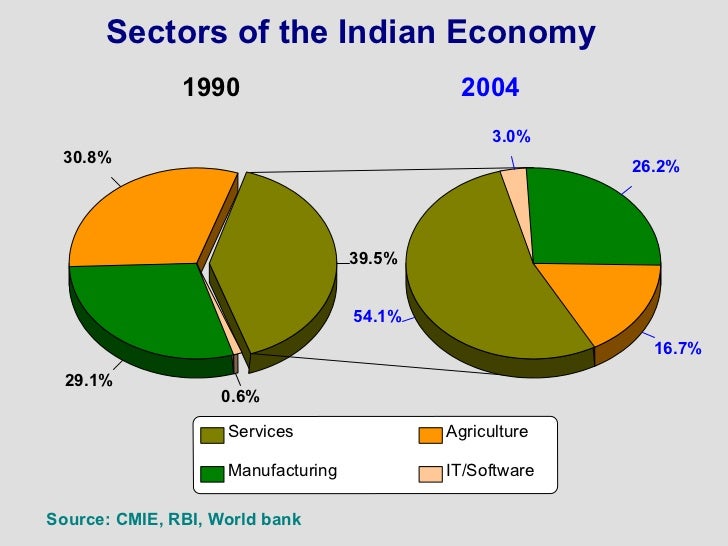

The economic reforms initiated by Prime Minister Narasimha Rao and his Finance Minister Manmohan Singh early 1990s dramatically changed the composition of the economy. The Services sector grew dramatically 38% to 54% and is now about 60% of the GDP mostly made up of Information Technology (IT) and Consulting making India the IT hub of the world. With the vaccine production for the Covid-19 virus, India is also emerging as the Pharmaceutical hub of the world.

The ten years under the economist Prime Minister Manmohan Singh between 2004-2014 were ridden with corruption in the first five and inaction in the second five. The first five saw artificial growth spawned by socialist government spending resulting in very high inflation rates resulting in deficits bringing down the value of the currency. The second half saw plummeting growth rates due to inaction of a government that was out of ideas, money, and vigour.

In 2014, Narendra Modi became the Prime Minister on the promise of zero-corruption, development based on minimal government and maximum governance, low-inflation, and business-friendly policies. In the first tenure of five years, there was no high-level corruption and initiation of several policies to empower citizens-- such as creation of hundreds of millions of bank accounts to transfer benefits directly and eliminating middlemen, better power management so there is ubiquitous energy availability, dramatic reduction of inflation, sharp spike in growth etc, availability of cooking gas, strong action against terrorism from Pakistan, etc. The Modi government also introduced two unexpected shocks to the economy. One was the unanticipated invalidating of large currency notes because of excessive fake note injection by Pakistan to terrorists in India. The other was a completely botched GST tax implementation. Coming one after another, growth plummeted for two years but inflation was low. In 2019, Modi won by even larger margins because of lack of corruption, sincere efforts to bring development, and also how he dealt with terror from Pakistan. The second term started great but was hit by the Chinese origin Covid-19 virus pandemic. The Modi government has injected several billions of dollars into the economy in multiple stages and it looks like the economy has already made a V-shaped recovery.

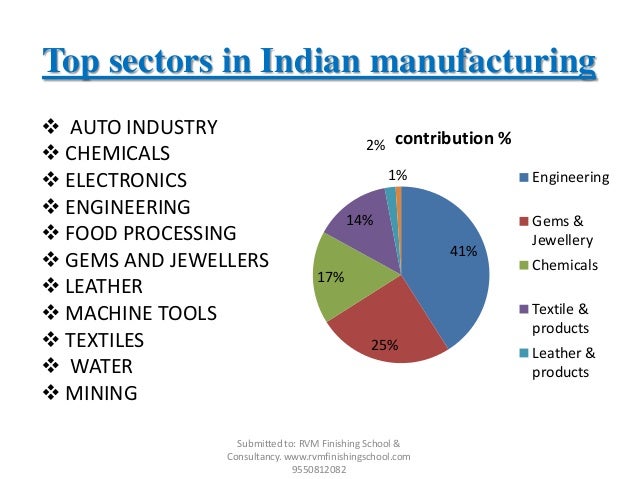

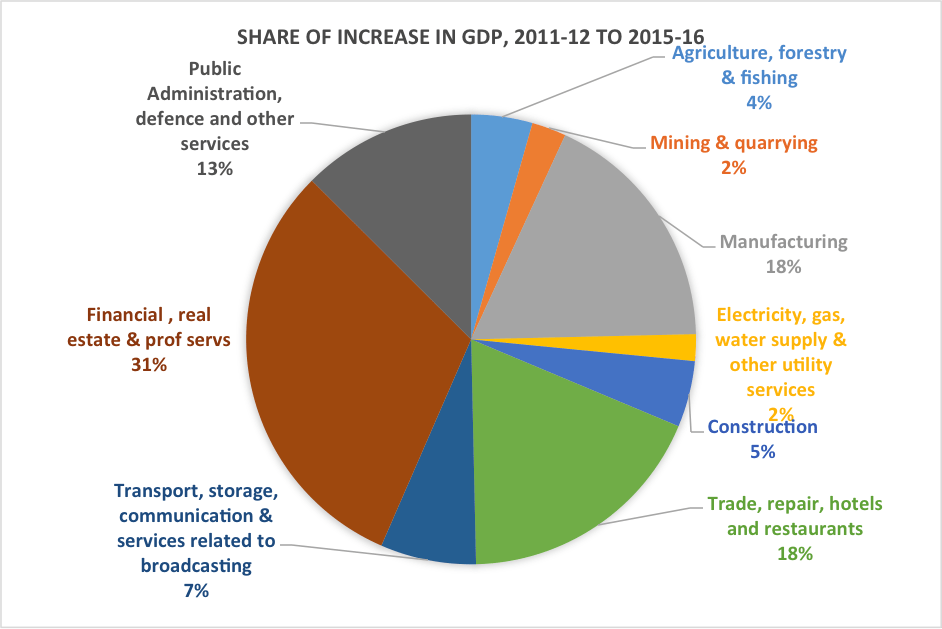

Agriculture provides employment to about 50% of the labour force followed by Manufacturing, Construction, and Trade. In terms of Gross Domestic Product (GDP), Services is the largest revenue earner netting more than half of all revenues followed by Industry and Agriculture. Aviation, Banking and Services, Financial, Information Technology, Insurance, Retail, Tourism, Media and Entertainment, Healthcare, Logistics, and Telecommunication are the major Services. Mining, Iron & Steel, Construction, Defence, Electricity, Engineering, Gems and Jewellery, Infrastructure, Petroleum Products and Chemicals, Pharmaceuticals, Textile, Pulp and Paper are the major industries out of India.

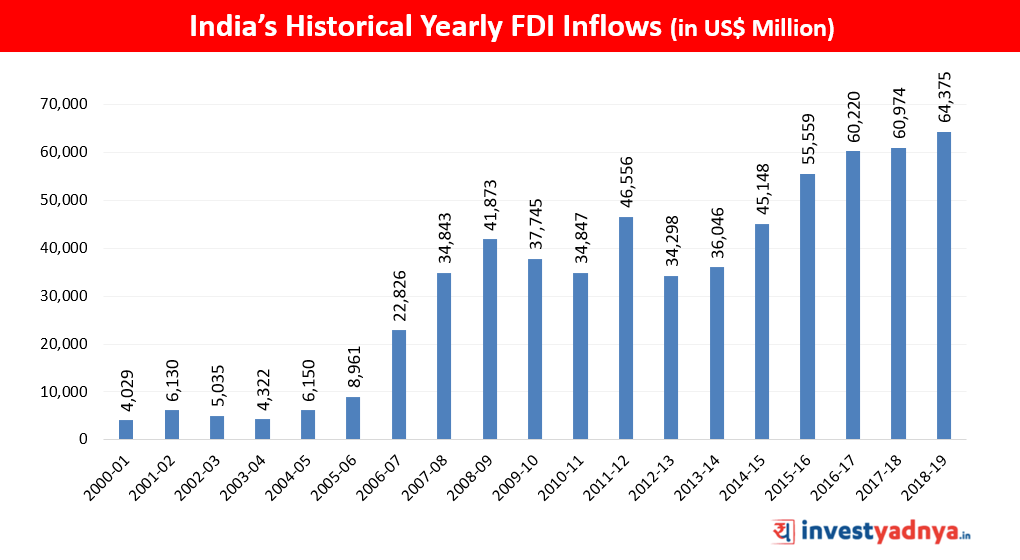

Petroleum products, Information Technology, and Gems & Jewellery make up more than 60% of Indian exports and Crude Oil, Electronics, and Gold make up more than half all imports. Before 1991, most of the foreign direct investments (FDI) were financial aid, commercial borrowings, and remittances from Indian expatriates. Post liberalisation, FDI inflows into various industries sky rocketed despite restrictions on investment limits. By 2015, foreign trade accounted for about 48.8% of the GDP. As a founding member of the General Agreements on Tariffs and Trade (GATT) and its successor the World Trade Organisation (WTO), India has been a vocal member representing the interests of developing nations including the addition of labour, environmental, human rights issues, and other non-tariff trade barriers.

About 42% of FDI comes from Mauritius, which is a tax-haven giving anonymity to investors including unscrupulous ones. This is a source of worry as India has a no-ask policy with Mauritius and Singapore and more than half of FDI comes through these countries. However, FDI is only 2% of the GDP. Indian companies also invest abroad and the outflow of FDI is about 1.3% of the GDP. Remittances from expatriates account for about 3% of the GDP mainly from UAE, the US, and Saudi Arabia.

FDI in India have spanned multiple industries including energy, construction, tourism, ecommerce, textile, education, gems and jewellery, hospitals, automobile and components, pharmaceuticals, agriculture and food processing, retail, mining, leather, capital goods, and media. Even in these pandemic times, most of these have reported great success. These projects not only generated profits for investors but also employment. The Make in India and the recently launched Atma Nirbhar (self-reliance) programmes have attracted a huge exodus of manufacturing investments fleeing China. In 2020-21, the relaxation of FDI norms in the defence sector more than USD 43.5B has already flowed in into just Reliance Jio Platforms (equal to what came in 2018-19 for the whole country). As a result of multi-layer reforms, India’s rank in the World Bank Doing Business report jumped to 63rd from 77 just a year ago.

However, some analysts point out that India needs to still fix problems foreign investors such as inconsistency in interpretation of laws, frequent changes to the laws, and lack of coordinated approach among different regulators in the country.

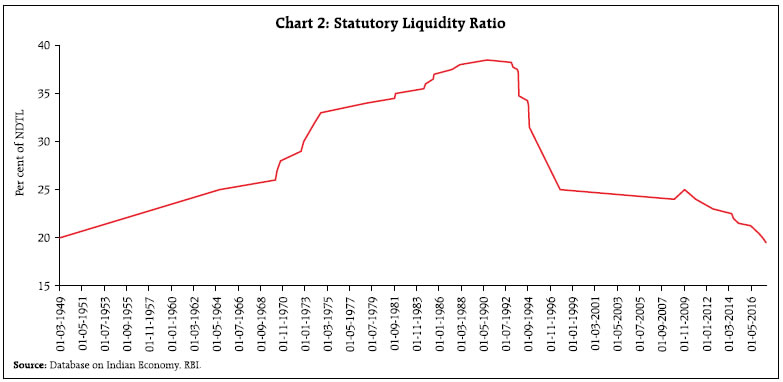

Established on April 1, 1935, the Reserve Bank of India (RBI) is the nation’s central bank managing monetary authority, regulator and supervisor of the monetary system, banker to the government, custodian of foreign exchange reserves, and as an issuer of currency (the Indian Rupee ₹). Managed by a Governor and a board appointed by the federal government, the body also sets the benchmark interest rates. The Rupee is a fully convertible currency on the current account albeit with some capital controls.

About

India has the third largest economy in purchasing power parity terms valued at USD 10.2 trillion. With over 500 million work pool, India has the second largest labour force with the second largest female technological workforce. According to Angus Maddison’s study on world economy, in the last 2,000 years, India was the largest economy for 1,500 years and then the second largest till 1800 till the British set up the Raj. When India gained independence, its share of the world economy was 3.8%.